When you decide that you’re going to manage rental properties, it’s important that you find the right accounting solution. You’ll likely need an accounting system in place to track rent payments, security deposits, net profits, expenses, and more. Even a spreadsheet for start.

The thing is, there is not just one solution that fits all. Instead, there are several different options that can help you track your finances, and which one you use will depend on your rental business.

In this article we’ll focus on what property management software is, how it can help with accounting, and how it compares to the popular financial app, QuickBooks. So, if you’ve been wondering if you should invest in Quickbooks vs. property management software, read on.

TL;DR

- QuickBooks is powerful accounting software built for general businesses.

- Property management software is designed specifically for rental operations and includes accounting plus leasing, rent collection, maintenance, and reporting.

- Small landlords with a few units may find QuickBooks sufficient, but overall, growing portfolios, owner reporting, and operational efficiency typically require property management software.

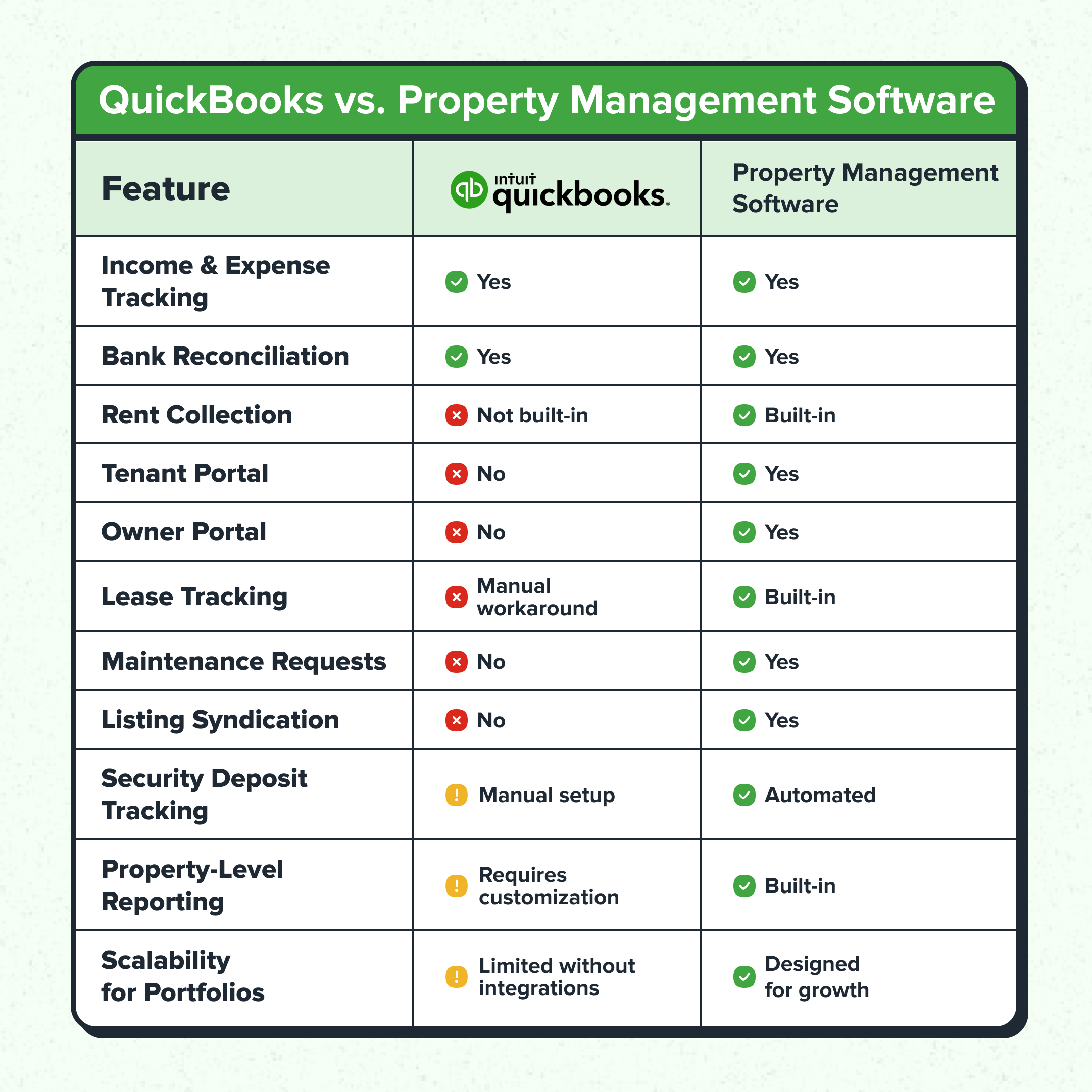

Comparing QuickBooks vs. Property Management Software

Feature | QuickBooks | Property Management Software |

Income & Expense Tracking | ✅ Yes | ✅ Yes |

Bank Reconciliation | ✅ Yes | ✅ Yes |

Rent Collection | ❌ Not built-in | ✅ Built-in |

Tenant Portal | ❌ No | ✅ Yes |

Owner Portal | ❌ No | ✅ Yes |

Lease Tracking | ❌ Manual workaround | ✅ Built-in |

Maintenance Requests | ❌ No | ✅ Yes |

Listing Syndication | ❌ No | ✅ Yes |

Security Deposit Tracking | ⚠️ Manual setup | ✅ Automated |

Property-Level Reporting | ⚠️ Requires customization | ✅ Built-in |

Scalability for Portfolios | ⚠️ Limited without integrations | ✅ Designed for growth |

What Is Property Management Accounting?

Like most businesses out there, you need to be able to keep track of your money going in and out. This includes what you are paying, what you are being paid such as rental payments, and how well your rental properties are doing overall. As such, you’re going to need a good accounting system to help you do this.

The more thorough and detailed records you have, the better position you will be in when it comes time for tax season, comparing rental properties, or creating reports for owners. A good accounting system helps you easily track the success, and potential failures on the monetary side, helping you to make better decisions moving forward.

Additionally, a good accounting software can streamline this process for you, so your payments and financial details are all in one place.

What is QuickBooks and How Does It Work?

QuickBooks is accounting software designed to help businesses track income, expenses, and overall financial performance. Developed by Intuit, it’s widely used by small businesses to manage bookkeeping tasks like invoicing, expense tracking, payroll, bank reconciliation, and financial reporting.

At its core, QuickBooks works by organizing your financial activity into categories. You connect your bank accounts and credit cards, and transactions automatically feed into the system. From there, you categorize income and expenses, generate reports like profit and loss statements or balance sheets, and reconcile your books to ensure everything matches your bank records.

For property managers, QuickBooks can help track rental income, vendor payments, maintenance expenses, and owner disbursements. It allows you to create financial reports for property owners and monitor cash flow across your portfolio. However, because QuickBooks is general business accounting software — not property-management-specific — it often requires customization, workarounds, or integrations to fully handle things like lease tracking, rent rolls, or tenant-level reporting.

In other words, QuickBooks is a powerful accounting engine. But on its own, it doesn’t manage properties.

Why Some Landlords Prefer QuickBooks

As QuickBooks was designed for accounting, it does have strong financial tracking, allowing you to follow everything easily. On top of this, QuickBooks has added a feature by which you can categorize your income and expenses by property, allowing you to easily see which of your rental investments are profitable.

QuickBooks may be a good fit if:

- You own 1–3 rental properties

- You primarily need tax-ready financial reports

- You are comfortable customizing chart of accounts

- You don’t need tenant or owner portals

- You’re okay managing leases and maintenance outside your accounting system

For independent landlords who want straightforward bookkeeping, QuickBooks can work well — especially in the early stages.

Limits Of QuickBooks

One of the main issues that it has is that it’s strictly for accounting, and this means that you’re not getting all of the added extras that you need to ensure that you are the best possible property manager or landlord. You don’t get things like a tenant portal to help your tenants keep track, and to help you keep track of them, it’s all just bundled together in numbers. What it offers is basic accounting for businesses, which is why it’s one of the most widely used accounting solutions out there.

You will also find that it is unable to separate business activity in the way that you need it to. What we mean by this is that property management companies have two sides to their business – the property management activity, and the financial activity. Unfortunately, QuickBooks simply doesn’t have the ability to manage both sides, and this will become more of a prevalent issue the larger your business or portfolio grows.

Why Landlords Prefer Property Management Software

First and foremost, the specialized software tends to have a tenant portal, as well as an owner portal that allows for easier overall management. Tenants are able to use this to pay their rent, communicate with you if needed, and get rental insurance (not on all types of software). Having this extra feature makes life so much easier, as everything is in the same place, it’s easy to use, and you don’t have to worry about a thing.

As with most things, there are certain pieces of rental property management software that have more features than others, which is why it’s so important that you complete your research and don’t just opt for the first one that you come across.

Property management software is better suited if:

- You manage multiple units

- You work with property owners

- You need automated rent collection

- You want tenant communication in one place

- You require lease tracking and rent rolls

- You want maintenance workflows built in

- You plan to grow your portfolio

Once operations move beyond “basic bookkeeping,” purpose-built systems become significantly more efficient.

Cons of Property Management Software

As with any new piece of software, there is going to be some sort of learning curve. You need to import all of your data, learn how to use the software that you choose, and then train any staff that you have working for you to use it also. This is a time consuming process, but once this initial setup and learning is done, it shouldn’t be too difficult to use.

The last point we want to make here is that there are some options that make integration with other pieces of software (if you decide that this is something you’re interested in) hard. On top of that, property owners may find themselves paying for features that they don’t actually need or use, which then turns out to be a bit of a waste of your finances. However, when using a more specialized solution, you would expect better features than a general accounting software, and that is exactly what you get.

Is There Truly an All-in-One Accounting Solution?

This is a tricky one to answer, because technically yes, both are all in one solutions – it just depends on what you are looking for. If you’re looking for something that can manage both the accounting and the property management side, then you’re going to need dedicated property management software, right? But, if you’re more interested in tracking the finances and keeping your eye on the accounts, and your business or portfolio isn’t that large, then QuickBooks could be a good solution.

What we have seen some people do is use both at the same time. It might be true that you feel like you need the flexibility and the features of a property management software, but that you also want the dedicated accounting that QuickBooks offers. If this is true, then you can use a combination of both to achieve the results that you want.

However, it’s also true to say that one is more of an all encompassing solution than the other, and that is the rental property management software. How could it not be, when it was specifically designed for cases such as this. It goes beyond basic accounting in a way that QuickBooks is unable to.

Best Financial Tools for Property Management

The answer depends on how complex your property management operation is — and how much manual work you’re willing to take on.

QuickBooks is a powerful accounting tool. It’s excellent for tracking income and expenses, reconciling bank accounts, running profit and loss reports, and managing payroll. For independent landlords with just a few units — especially those already familiar with accounting systems — QuickBooks can be a solid foundation.

However, property management has layers that go beyond standard bookkeeping. Tracking leases, managing security deposits, handling tenant charges, organizing maintenance expenses by property, generating owner statements, and syncing rent payments directly to accounting records requires more than general accounting software. With QuickBooks, many of these workflows require customization, spreadsheets, or third-party integrations.

That’s where property management software stands apart. Platforms designed specifically for rental operations combine accounting with rent collection, lease tracking, listing syndication, maintenance workflows, and reporting — all in one system. Instead of adapting accounting software to fit real estate, you’re using software already built for it.

If your priority is clean books, QuickBooks does the job well. If your priority is running a streamlined, scalable property management business, a purpose-built platform may offer far greater efficiency.

Which Is Best? QuickBooks or Property Management Software

If you’re managing one or two properties and simply need reliable accounting, QuickBooks can work. It’s familiar, established, and trusted for general bookkeeping.

But if you’re actively growing a portfolio, working with property owners, or managing multiple units, the better question becomes: Do you want accounting software — or do you want a complete property management system?

Property management isn’t just about tracking dollars. It’s about tracking leases, tenants, maintenance requests, marketing performance, and owner communication — all while keeping financials accurate and accessible. When those systems live in separate tools, the gaps show up in your time, your stress level, and sometimes your bottom line.

In most growing property management businesses, the all-in-one approach wins. It reduces manual processes, eliminates double data entry, improves reporting transparency, and creates a more professional experience for owners and tenants alike.

Final Thoughts

There is no one-size-fits-all answer to the QuickBooks vs. property management software debate.

If you simply need clean books for a small portfolio, QuickBooks may be enough. But if you’re building a property management business — handling leases, tenants, maintenance, owner reporting, and growth — then accounting alone won’t carry the weight. You need a system built specifically for rental operations.

Frequently Asked Questions: Accounting Software

Can QuickBooks be used for rental properties?

Yes. QuickBooks can track rental income, expenses, and generate reports. However, it does not include property management features like rent collection portals, lease tracking, or maintenance management without additional tools.

Is property management software more expensive than QuickBooks?

It depends on the provider and portfolio size. QuickBooks has subscription tiers, while property management software may use flat-fee or per-unit pricing. While property management platforms can cost more upfront, they often reduce time, manual processes, and the need for additional software.

Can I use QuickBooks and property management software together?

Yes. Some landlords use property management software for operations and QuickBooks for high-level accounting. However, many modern property management platforms include robust accounting features, eliminating the need for separate systems.

What’s the biggest limitation of QuickBooks for landlords?

QuickBooks was not designed specifically for property management. Lease tracking, tenant-level reporting, rent rolls, and maintenance workflows require customization or third-party integrations.

Does property management software handle taxes?

Most property management platforms provide tax-ready reports such as profit and loss statements, rent rolls, and expense summaries. Some also assist with 1099 generation and owner statements.