Property values change over time, and come tax season, rental owners use that to their financial advantage. One of the most important tax deductions for landlords is rental property depreciation. By calculating the reduction in property value over the years and deducting it, owners can save on their taxes.

All in all, it allows them to reduce their tax bill to make the most of their rental income. In some cases, it even allows landlords to drop into a lower tax bracket, enabling them to access even more savings. However, you need to meet certain qualifications before you claim the rental property depreciation deduction.

TL;DR

Rental property depreciation is a deduction strategy landlords use to reduce their taxable rental income. The process works by spreading the costs of rental ownership over a set period of time, typically 27.5 years. When filing your taxes, report depreciation on Schedule E to maximize your rent collection income and access more savings.

There are a few different ways to approach depreciation, including the General Depreciation System (GDS) and the Alternative Depreciation System (ADS). Remember, rental property depreciation can help you save today, but it may trigger recapture taxes if you sell the unit without using a 1031 exchange strategy.

Overview: Rental Property Depreciation and Rental Income

Rental property depreciation is the drop in a property’s value that happens over time. As a landlord, you can claim depreciation as a tax deduction to maximize your rental income.

When you purchase a new unit for your portfolio, you pay a large lump sum up front. To make up for this investment, the IRS allows owners to offset the cost of the property by considering its reduction in value over the years.

However, you can’t write off the entire purchase amount every year. Instead, you must spread the deduction out over the investment’s lifespan. In general, ownership expenses align with the income generation period.

According to the IRS, rental properties lose about 3.6% of their value every year. Naturally, a unit doesn’t stay in perfect condition forever. Normal wear and tear and aging impact the asset’s value, and depreciation is a check-and-balance system that considers the returns and long-term expenses.

When it comes to reporting your income, rental property depreciation reduces your total profit and your tax burden. By taking your losses into account, you save each year. Landlords use the Modified Accelerated Cost Recovery System (MACRS) to calculate depreciation for accurate tax filing.

Eligibility to Depreciate Residential Rental Property

You have to check off a few boxes before you use rental property depreciation to balance your profit and loss. To claim depreciation on your units, you must meet these three IRS conditions:

- You own the property.

- You use the property to generate income in some way — whether you rent it out to tenants or use it for business purposes.

- Additionally, the unit should have a useful life that’s longer than 1 year.

Even if you purchased the property with a mortgage, you’re still considered the owner. In other words, you can claim depreciation even as you pay your mortgage bill every month.

However, you can’t claim the full year’s depreciation if you don’t use the property to generate profit for the entire year. For example, if you only lease it from January to April, you don’t qualify for 12 months of depreciation.

Additionally, you can’t rent the unit out to yourself where you’re the tenant, or sublet the unit to someone else. The bottom line? If the property’s main function is personal use, you can’t claim the depreciation deduction.

Lastly, you must consider land-related costs as separate from the property’s depreciation. You can’t add clearing, planting, or landscaping bills unless they’re related to the depreciable property. If you have specific questions about whether or not a land-specific cost qualifies, we recommend speaking to a trusted financial expert about these exclusions.

When Depreciation Begins and Ends for Rental Properties

When does the depreciation period begin? It starts on the in-service date, or when you begin using the property to generate profit. Remember, the in-service date isn’t the date when you close on the property’s purchase. It’s when the unit is rent-ready. Even if a tenant hasn’t moved in yet, as long as the unit is listed on the market, you can start the clock.

Let’s say you purchase fixer-upper houses and you intend to spend time conducting renovations and repairs. In this case, you must wait until you’re ready to give tenants the key and start a lease before depreciation begins.

Rather than using exact days, the IRS uses a mid-month rule to make the organization easier. If you list your rental on April 4 or April 24, you still get the same partial-month depreciation. By assuming a middle-of-the-month activation, you don’t have to calculate specific days or navigate any gray area.

Depreciation ends when you remove the property from service or stop using it to generate income. This happens when you sell the unit, start occupying it for personal use, or stop renting it out altogether.

Whether you move into the home or take it off the market until further notice, you lose the right to claim depreciation. Even if you plan to rent it out again later, you must stop the clock until you officially put it back on the market.

Cost Basis, Allocation, and Annual Depreciation

The first step to calculating your rental property depreciation is to understand your cost basis. The cost basis refers to the total amount you paid for the property, including the purchase price, legal fees, and title insurance.

Make sure to separate your cost basis for the property and the land. When determining your depreciation tax deduction, you can only use the cost basis for the actual property. As a best practice, consider speaking with a professional appraiser or checking your property tax assessment to allocate the funds correctly.

Next, figure out what your annual depreciation is. If you’re using the General Depreciation System (GDS), which is the most common, you use a 27.5-year recovery period with a straight line method. We’ll explain the GDS in detail, but here’s a quick overview of how to calculate your annual depreciation:

- Step 1: Subtract the value of the land from the cost basis to determine the depreciable basis.

- Step 2: Divide the depreciable basis by 27.5 years to get your annual deduction amount.

Let’s say your depreciable basis is $300,000. $300,000 divided by 27.5 equals an annual depreciation of $10,909.

Cost Recovery System MACRS and Method Choices

To depreciate a residential rental property in the U.S., owners use the Modified Accelerated Cost Recovery System (MACRS). As mentioned, MACRS sets a baseline recovery period of 27.5 or 30 years to standardize the calculation for tax purposes.

Landlords can choose two different approaches to MACRS for their tax filing. There’s the General Depreciation System (GDS) and the Alternative Depreciation System (ADS). Once you choose, you have to stick with it for the lifetime of your property. You can’t change from the GDS to the ADS, or vice versa, halfway through the depreciation period.

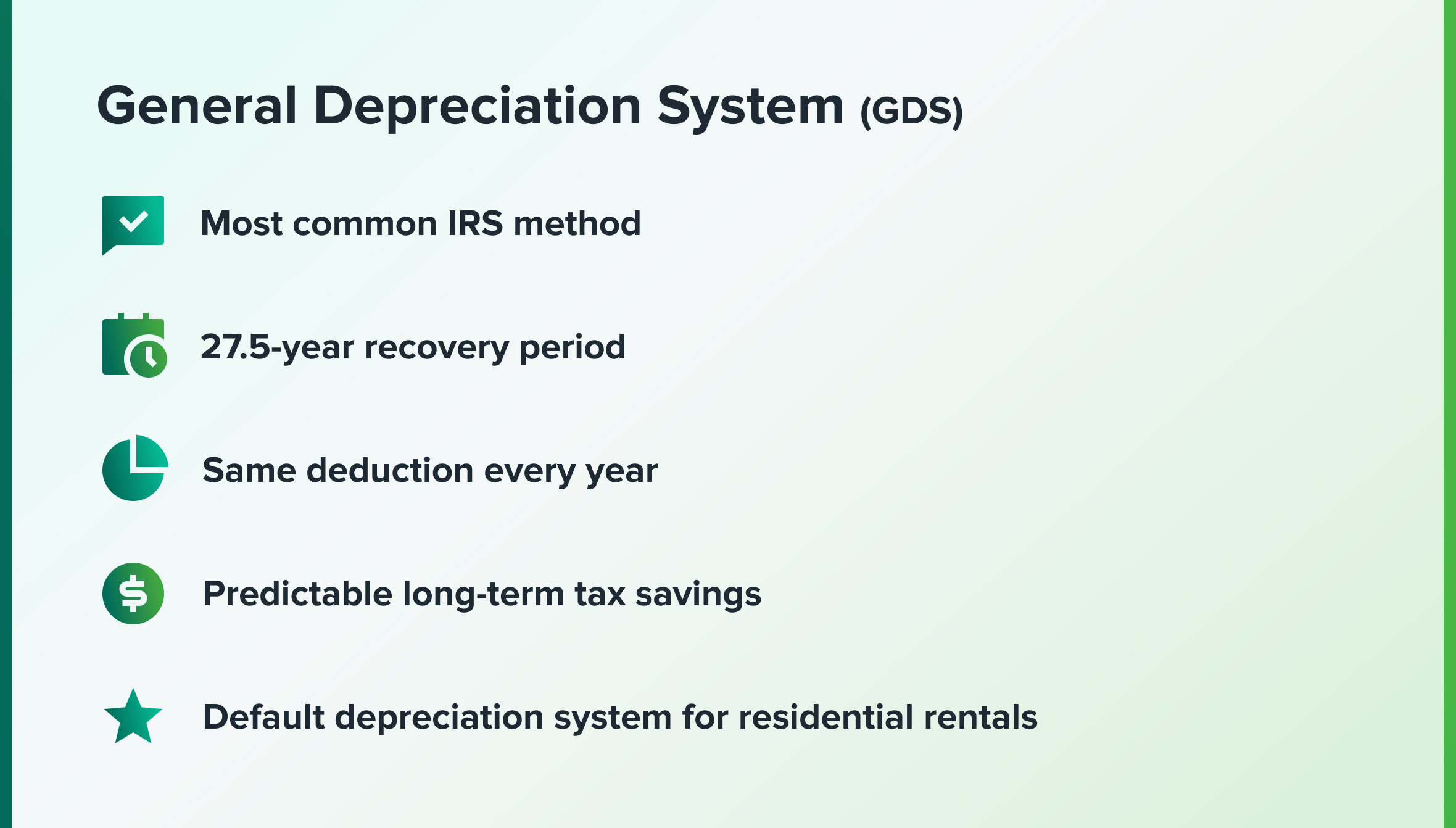

General Depreciation System (GDS) — General Depreciation System GDS

Most owners use GDS, which provides a recovery period of 27.5 years for residential properties using a straight-line depreciation method. In other words, the depreciation rate stays the same every year. With the GDS, you get the same deduction each year for the full recovery period.

GDS is the default approach set by the IRS. If you want to use the ADS, you have to specifically mark your decision.

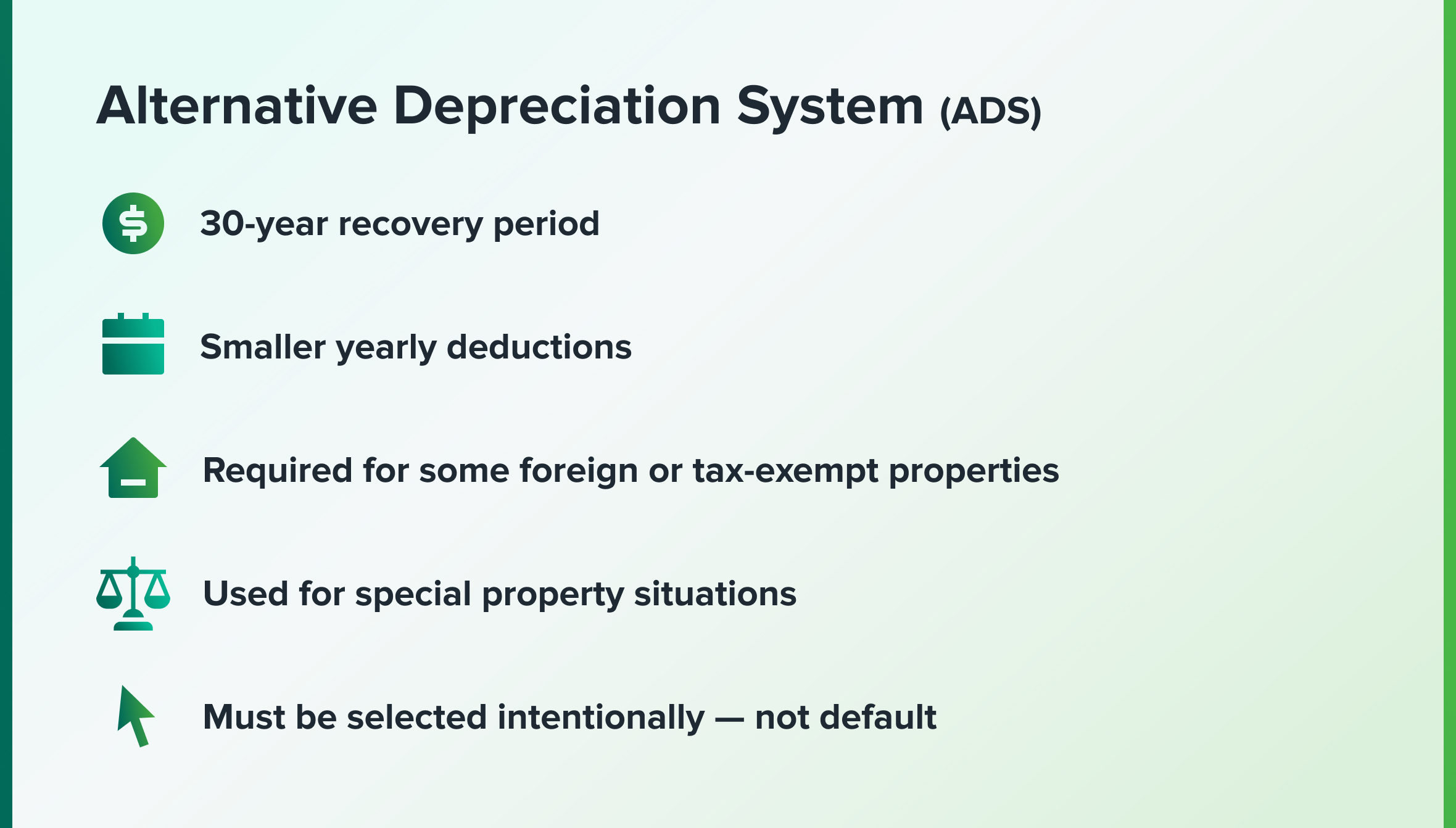

Alternative Depreciation System (ADS) — Alternative Depreciation System ADS

On the other hand, the ADS uses a 30-year recovery period and a straight-line deduction calculation. Because ADS sets a longer lifespan, you end up getting a smaller depreciation amount for a longer period compared to GDS.

Some properties are required to use the ADS system, such as:

- Tax-exempt units

- Properties owned by business entities (such as real estate investment trusts)

- Units financed with tax-exempt bonds

- Properties used outside of the U.S.

- Properties used by foreign individuals or entities that don’t pay U.S. income taxes

If you’re unsure about whether or not your property requires the ADS system, consult a trusted real estate or financial advisor.

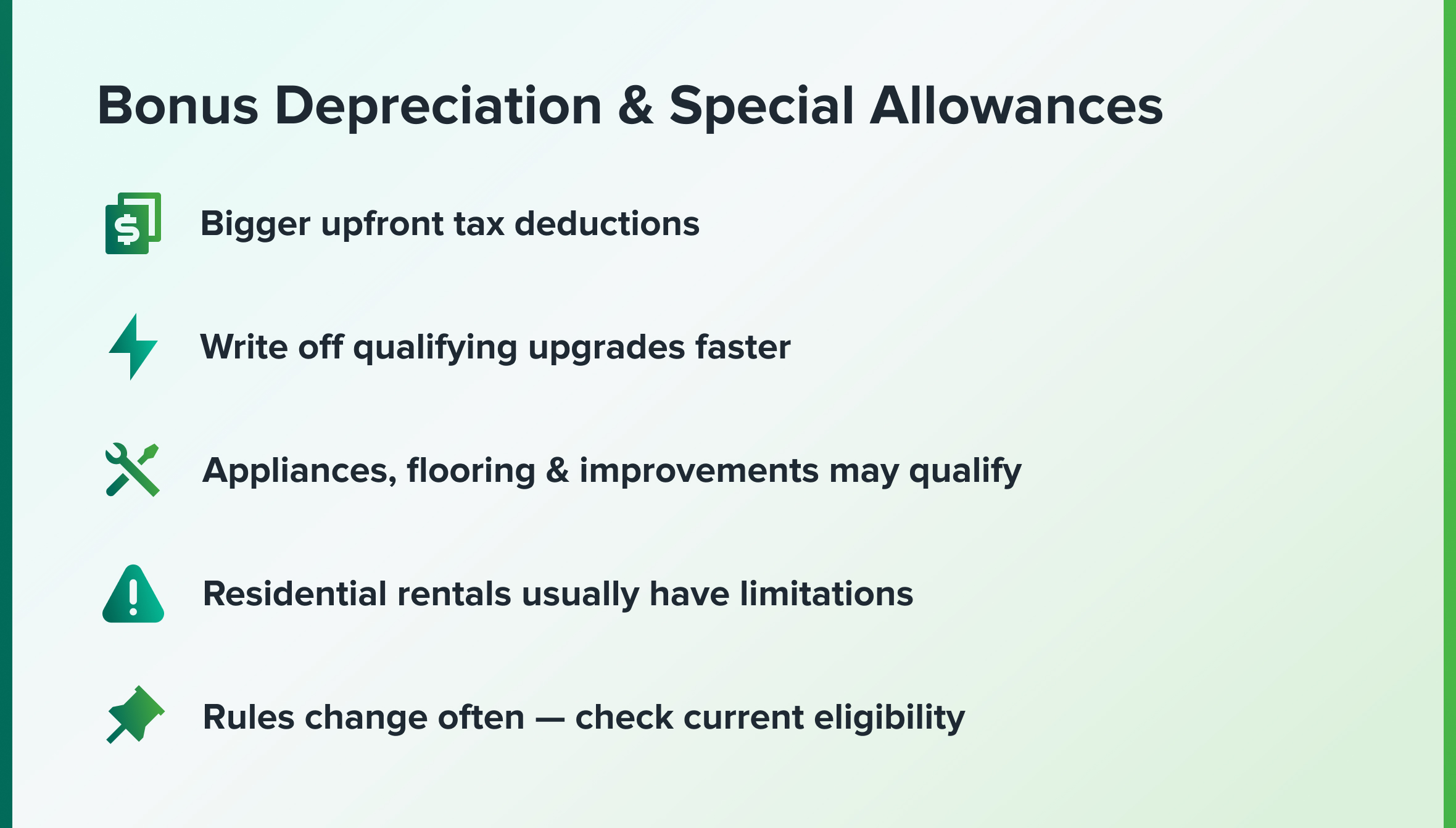

Bonus Depreciation and Special Allowances

In some cases, you don’t have to spread rental property depreciation over three decades. Instead, landlords may be able to speed up and increase their tax deductions by writing off all or most of the asset’s purchasing cost in the first year the property’s in service.

According to both MACRS systems, residential properties don’t usually qualify for bonus depreciation or special allowances. However, you may be able to claim the accelerated deduction based on items in the home with shorter recovery periods, such as appliances, flooring, or other specific property upgrades you invested in.

Bonus depreciation is a great way to maximize upfront tax savings if you qualify for them. Remember to always check your eligibility for bonus rules in the current tax year, as they change frequently.

As with any tax-related questions, get specific guidance by speaking with a tax professional. Otherwise, you may end up paying for expensive errors for small mistakes.

Annual Depreciation Calculation Examples

Let’s take a closer look by running the numbers for a few common rental property depreciation calculations.

Full-Year Straight-Line Depreciation

You purchase a rental property for $315,000, rent it out for an entire year, and determine that $275,000 went to the actual structure. You’re using the GDS, which splits depreciation over 27.5 years using a straight-line method.

To calculate your annual depreciation amount, divide $275,000 by 27.5. In this example, you can deduct $10,000 each year from your taxable income.

Partial-Year Mid-Month Depreciation

Let’s imagine you had the same property and put it on the market on March 12. In this case, the IRS treats the unit as if you placed it in service in the middle of March. With the mid-month convention, you deduct a pro-rated amount from the full year’s depreciation to account for the months it was in service.

In this example, you could claim 9.5 months of depreciation to cover the months from Mid-March to December. First, divide 9.5 by 12 to determine the pro rate, which equals 0.79. Then, take the property’s annual deduction of $10,000 and multiply it by the sum.

$10,000 multiplied by 0.79 equals $7,900, which is your deduction for that year when the property was in service from March to December.

Asset Improvement Depreciation

2 years later, you install new flooring in the property for $6,000. You can also apply depreciation for capital improvements, and you track it as a separate asset on your taxes. While some upgrades qualify for shorter recovery periods, many still use the 27.5 timeline.

In this case, divide the project’s cost of $6,000 by the recovery period of 27.5 to calculate your annual deduction, which is about $218.

Regardless of the depreciation time, always remember to consider each improvement individually and run it on its own timeline.

Reporting, Forms, and Tax Savings for Properties That Generate Income

When it comes time to do your taxes, always file rental property depreciation on your IRS Schedule E (Form 1040). But in the first year the property’s in service, you must also file a Form 4562. This form submits the qualified properties to the IRS and kicks off the depreciation period for your rental units.

To make the most of your tax savings, we recommend documenting depreciation. Keeping an organized paper trail makes filing fast and easy while boosting your returns.

It’s also a good idea to track improvements for separate depreciation. If you replace a roof or install new flooring, avoid lumping what you spend on upgrades into the property’s original value. Logging them as separate assets keeps your tax records clean for audit protection. It also allows you to qualify for faster depreciation or bonus depreciation, since some investments qualify for special allowances.

Let’s say you install a new HVAC system 4 years after purchasing a home. If you spend $9,500 on the property upgrade, track it separately and depreciate it on its own schedule. Don’t combine it with the original amount you spent on the property when buying it.

Depreciation Recapture, Sale, and Rental Income Implications

Planning to sell your property? Don’t forget about depreciation recapture. The IRS requires rental owners to pay tax on the depreciation they claimed when they owned their units. In most cases, rental property depreciation is taxed at a higher rate than long-term capital gains, which can cut into how much you walk away from the sale with.

Before the sale, calculate your adjusted basis to get a better understanding of what your gain will be. Start by taking the original purchasing price and adding the cost of any upgrades you made. Then, subtract all depreciation deductions you claimed throughout the life of the property to get the adjusted basis. To determine your total taxable gain, compare the adjusted basis to your sale price.

Rather than facing a large tax bill at the time of sale, many investors protect their income by using a 1031 exchange strategy to defer taxes. With a Section 1031, you opt to reinvest the funds you generate from the sale into another similar investment asset. Doing so defers both depreciation recapture taxes and capital gains, so you’re not paying out of pocket right away.

If you’re interested in taking the 1031 exchange route, start planning the transactions early. You must meet strict timelines and comply with specific rules, so it’s a good idea to work with an expert to keep you compliant every step of the way.

Common Mistakes to Avoid with Rental Properties Depreciation

All things considered, depreciation is a great way to reduce your taxable income, generate annual savings, and recoup what you invested to buy a property. However, you can only reap the full benefits when you do it correctly.

When adding rental property depreciation to your tax strategy, pay special attention to avoid common errors many landlords make. Here are a few examples to look out for:

1. Make sure you claim your allowed depreciation every year.

Don’t skip the depreciation to try and save it for later, because you can’t. The IRS restricts depreciation by labeling it as “allowed” or “allowable.” As a result, you pay taxes on it when you close on the sale, whether you claim it or not. And if you don’t apply it annually, you miss out completely. Plus, you still need to pay depreciation recapture if you sell the property in the future.

If you make a mistake and forget to apply the depreciation deduction, don’t worry. Correct the error by filing for a correction using the official IRS process.

2. Avoid mistakes when separating land and building values.

Remember, land can’t be depreciated. You can only claim deductions on what you spent on the actual building. If you allocate too much, you actually reduce your annual deduction amount. On the other hand, allocating too little can look like a red flag.

Err on the side of caution by using an official property tax assessment, rental property inspection, or appraisal to calculate the price of the land and the property.

3. Always keep detailed depreciation schedules.

Because depreciation is an ongoing record that spans decades, you need a strong paper trail to report accurately and boost your deductions.

As a best practice, create a depreciation schedule that tracks the original cost basis and its allocation. Be sure to add separate line items for any upgrades you make, taking note of the cost, date placed in service, and the recovery period. Keep a log of the annual depreciation you take alongside the total depreciation you accumulate over the years.

In conclusion, be consistent and document your rental property depreciation to make the most out of the deduction. Make sure you claim depreciation every year and keep detailed records to avoid issues and surprises down the line.

FAQs: How to Depreciate and Maximize Tax Savings

How many years does it take for a residential property to depreciate?

Based on the GDS system, landlords usually calculate rental property depreciation over 27.5 years. If you use the ADS system, use a recovery period of 30 years. Remember, both options work with a straight-line method where you deduct the same amount every year.

What happens if you don’t claim depreciation?

Skipping depreciation isn’t really an option. Even if you don’t collect a depreciation deduction, you still have to pay depreciation recapture taxes when you sell the unit. As a result, you miss out on potential tax savings, but you still pay on the “allowed” or “allowable” amount the IRS calculates.

When should you elect ADS versus GDS?

Even though GDS is the standard with a shorter recovery period and larger annual deduction amount, sometimes the IRS requires landlords to use the ADS system. Use ADS if it works for your tax strategy or to comply with requirements for:

- Tax-exempt units

- Properties owned by business entities (such as real estate investment trusts)

- Units financed with tax-exempt bonds

- Properties used outside of the U.S.

- Properties used by foreign individuals or entities that don’t pay U.S. income taxes

Resources: MACRS Tables, Forms, and Further Reading

- IRS Publication 946: MACRS tables

- IRS Publication 527: Rental rules

- IRS Form 4562: Instructions for depreciation reporting

Rental Property Depreciation FAQs

How much depreciation can I write off on a rental property?

Rental owners can depreciate the building’s structural value (not land) plus closing costs based on a 27.5-year recovery period. To calculate how much you can write off annually, first subtract the value of the land from the cost basis to determine the depreciable basis. Next, divide the depreciable basis by 27.5 years to get your annual deduction amount.

What happens after 27.5 years of depreciation?

After the 27.5-year timeline for GDS (or 30 years for ADS), the IRS considers the property as fully depreciated under the MACRS guidelines. Moving forward, you can’t collect a depreciation deduction anymore.

Is it worth it to depreciate rental property?

Yes! Depreciating your rental property reduces your taxable income and generates savings. If you don’t take the depreciation deduction, the IRS still taxes you on the amount when you sell it. By opting out, you end up paying taxes twice if you sell the unit.