Before renting out an investment property, you need to know if the person moving in can pay their rent without issues. This is where learning how to run a credit check on a tenant is essential. Think of it like a report card for how someone handles their money.

A credit report can show financial patterns, such as whether a prospective tenant has made late payments. These patterns can be an indicator of the applicant’s financial responsibility. As a landlord, the last thing you want is the hassle of chasing after rent or, worse, having to file eviction proceedings because they won’t pay.

A tenant credit check can help you avoid unpleasant legal action and unpredictable cash flow.

TL;DR

A tenant credit check helps you ensure timely rent payments and provides a glimpse of a tenant’s financial habits. Knowing their previous financial behavior can help you identify responsible tenants and protect your rental investment.

To conduct a successful and legal rental credit check, make sure to get written permission from the applicant, use a trusted screening service (like TenantCloud), and review the report carefully.

What Is a Tenant Credit Check?

First, what is a tenant credit check? When you think about a tenant credit check, you might assume it’s only a credit score. But it’s important to remember that a credit score is just one piece of the puzzle. When you pull a complete credit check of your potential tenants, you’ll often get a fuller picture. This means looking at their entire credit report to see the full story.

A tenant credit check is a financial review of an applicant’s credit history, usually pulled from a major bureau like TransUnion, Experian, or Equifax. Some purpose-built tenant screening services aggregate credit reports from multiple bureaus.

For any landlord, credit checks aren’t the only part of screening potential tenants, but they are one of the most important. Credit checks are one of the most reliable predictors of rent-payment behavior.

Landlords who skip credit checks in the tenant screening process face a 60–80% higher risk of eviction. That’s why we put together this step-by-step guide to running a credit check. We’ll cover red flags to look for, as well as thresholds for acceptable credit scores.

Why Landlords Should Run Credit Checks

A credit check for landlords is a way to assess how likely a tenant is to be reliable when it comes to paying rent. The report includes payment history and outstanding debts, which point to how healthy an applicant’s finances are.

Here are a few good reasons to include credit checks in your tenant screening process:

- Ensure reliable rent payments: A credit check can make it easier to determine if a tenant has a good track record of paying their bills. You want someone who will pay on time without needing constant reminders.

- Find responsible tenants: Their credit history gives you a picture of how a tenant manages their money. Do they spend wisely, or are they maxing out their credit card, resulting in bad credit?

- Spot red flags: Credit reports can help you identify other potential issues that are often red flags, like recent bankruptcies, multiple accounts in collections, prior evictions visible in public records, or vehicle repossessions.

- Keep criteria consistent: Using the same credit check rules for every applicant means a fair, equitable tenant screening process, and keeps you in compliance with the Fair Housing Act.

- Peace of mind: Finding a tenant with “green flags” like good credit can take some of the stress out of signing a new lease agreement.

- Legal documentation: In the event a credit report raises enough concern for you to reject an application, having the documentation on hand can make it easier to defend yourself against potential discrimination claims.

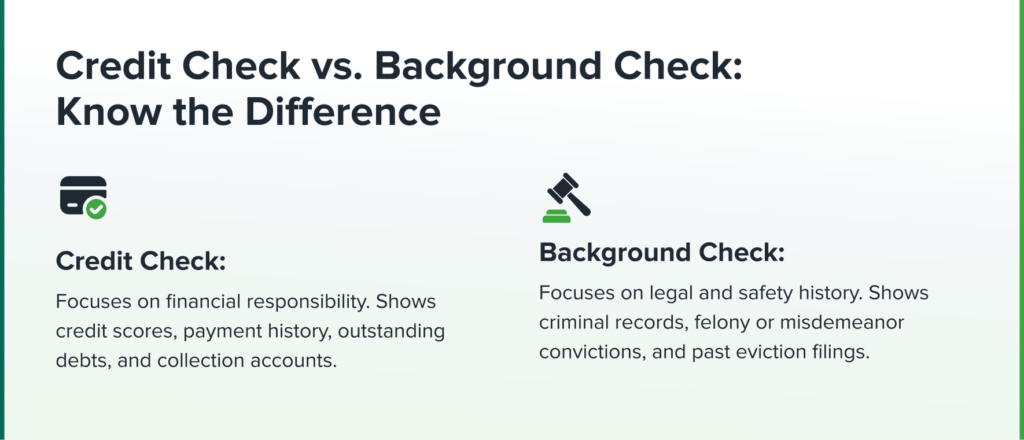

Tenant Credit Check vs. Tenant Background Check

A tenant credit check and tenant background check go hand in hand, but they’re two separate tools for landlords to assess potential renters. While each one serves a unique purpose, they are both crucial to the tenant screening process, and can provide a bigger picture overall when used in tandem.

So, let’s take a quick look at the differences:

Credit Check

A tenant credit check is mostly focused on how someone handles their finances. This report shows things like payment history (late or missed payments), debt, and overall credit score.

Background Check

A tenant background check, on the other hand, helps you identify an applicant’s criminal history. In addition to verifying identity, this report shows arrests, convictions, and eviction records. Prior convictions aren’t always a dealbreaker, but you should be wary of tenants with multiple arrests or a history of violence. Most checks come back within 1 to 5 business days.

Background checks can make it easier to vet tenants based on previous behavior, while a credit check can show how financially responsible they are. When it comes to finding the right tenant, both checks are equally important in the screening process.

To handle the credit and background checks in one easy-to-use workflow, platforms like TenantCloud bundle information from both checks into one simple report.

What Shows Up on a Tenant Credit Report

A tenant credit report covers several important pieces of data that, when combined, provide insight into their reliability when it comes to finances. The key components of a credit report include:

- Credit score: While this is only a single number, it’s a quick reference for signs of financial instability (more on what score ranges you should look for later).

- Payment history (35% of score): The largest part of a credit score is the ratio of on-time payments to late payments. This is one of the key indicators of a tenant’s ability to pay rent on time.

- Credit utilization (30% of score): This assesses not only total debt amount, but the percentage of debt types, which is also an important consideration (student loan debt is less of a red flag than high-interest credit card debt, for example).

- Length of credit history (15% of score): How long someone has been managing their credit plays a part in their credit rating. While this is less of a factor than debt and payment history, someone with a very short credit history may be harder to assess.

- Credit mix/new credit (10% each): It’s generally more desirable to see a few different types of credit (car loans, credit cards, etc.). Recently opened accounts aren’t necessarily red flags, but they can be a sign of financial instability.

- Public records: Credit reports also include legal records like bankruptcies, evictions, liens, judgments, and lawsuits.

How to Run a Credit Check on a Tenant (Step-by-Step)

Here’s how to run a credit check on a tenant, broken down into easy steps:

- Pre-screen your applicants: Before processing a credit or background check, first pre-screen your tenants. For instance, if a renter’s income must be 3x the rent, but they only earn 2x, this pre-screening answer would usually halt the application process before you take the time to run a credit check.

- Get permission: Always get written permission from the prospective tenant. This step isn’t just a courtesy; it’s a requirement of the FCRA (Fair Credit Reporting Act). You can do this through our online rental application form, included in your TenantCloud account.

- Choose a service: Pick a reputable tenant screening service or credit bureau that provides full credit reports, background checks, and income insights. (TenantCloud offers thorough tenant screening packages that check all the boxes.)

- Gather the details: Have the tenant’s personal details available, like their full name, address history, Social Security number, and birth date. Ideally, you’d want your applicants to fill in this information on their online rental application.

- Understand the costs: Running a comprehensive credit check costs money but it should be affordable. You’ll need to decide if you’ll cover these costs or if you’ll ask the tenant to handle the fee. You can set up the fees on your TenantCloud account however you like.

- Review the results: Once you have the report, take your time going over it. Our tenant screening reports give you all of the information you need to make an informed decision and help you find a great tenant.

- Keep reports confidential: This info is private. Make sure you keep it safe and don’t share it with others. This is easy to do on TenantCloud since only you should have the login information.

- Follow-up with the tenant: Consider talking to the tenant about any records that come up. Sometimes, there’s a good explanation for a past issue. If you decline an applicant after screening them, you’ll need to send them an Adverse Action Notice, per the FCRA.

- Stay consistent: Use the same process for every applicant. This helps you stay fair and avoid potential legal issues that can arise in the application process.

- Know the law: Brush up on laws like the Fair Credit Reporting Act and your local (state/city) regulations. For example, some states like New York (or individual cities like Seattle) have a unique set of laws that govern the tenant application screening process.

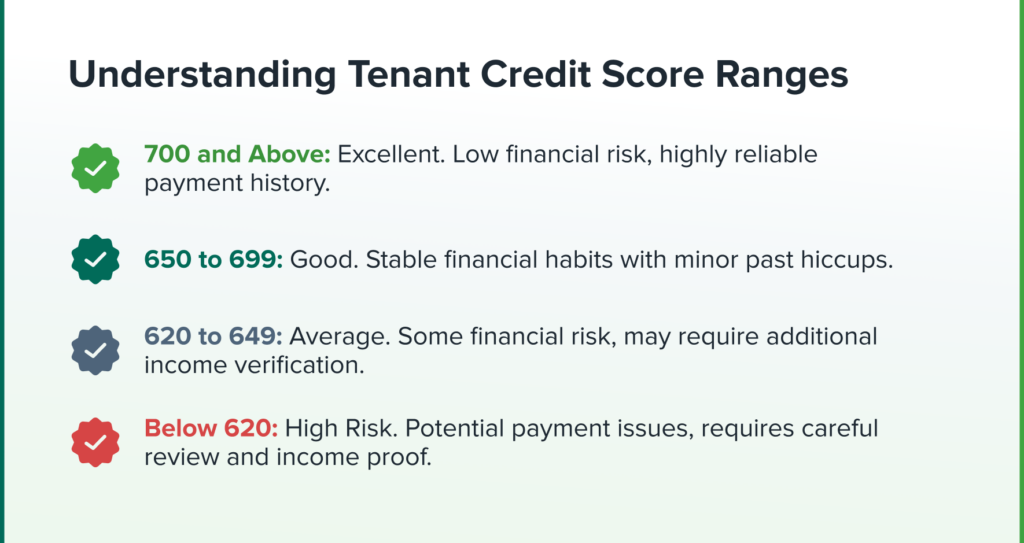

What Are Good Credit Scores for Tenants?

Here’s a general overview of credit score ranges:

| Credit Score Range | Category | Implications for Tenants | Typical Approval Odds |

|---|---|---|---|

| 800-850 | Exceptional | Highest reliability, best rental terms | Nearly certain |

| 740-799 | Very Good | Low risk, favorable leases, lower deposits | Very high |

| 670-739 | Good | National rental average, solid payment history | High |

| 650-669 | Acceptable/Fair | Common threshold, may need references or a higher deposit | Moderate |

| 580-649 | Fair | Riskier, often requires a cosigner, and a larger deposit | Low to moderate |

| 300-579 | Poor | High risk, application likely denied | Rarely approved |

Keep in mind that what qualifies as a “good” score varies meaningfully depending on the specific rental market. For example, luxury urban markets often require a score of 700 or more, while smaller markets might readily accept 620–650.

How to Read and Interpret a Credit Report

When you look at a tenant’s credit report, you’re looking at more than numbers. You should also look for the story those numbers tell. These are some of the biggest factors to consider:

- Look beyond just the score: One number is less important than the patterns reflected in a credit report. Just as a high credit score doesn’t always translate to a good tenant, you can’t rule someone out based just on a lower score.

- Check the debt-to-income ratio: A tenant’s credit utilization tells you how well they’ve got their finances under control. If they make enough money to comfortably cover the rent after their other bills, that’s a good sign. A ratio higher than 50% isn’t a dealbreaker, but consider it a yellow flag.

- Account standing: Look for any accounts that are overdrawn, maxed out, or in collections. Ideally, your tenant’s accounts should all be in good standing.

- Rental history items embedded in the report: Look for history details hidden in the report, like a history of late payments, past evictions, or money still owed to previous landlords.

- Recent credit inquiries: It’s common for applicants to have a few credit inquiries before getting into a rental unit if they apply to multiple properties. However, a large number of recent credit checks in a brief window of time can be a sign of financial stress.

- Fraud alerts: Particularly in applicants with lower scores, fraud alerts may indicate identity theft rather than poor money management, which can impact their score unfairly.

What If a Tenant Has Poor Credit or No Credit History?

In some cases, an applicant may have no credit history at all. Here are the four most common reasons for no credit history:

- They’re young and haven’t built a credit history (common in college towns).

- They’re wary of banks and haven’t built up a relationship with a financial institution.

- They’ve recently moved into the country.

- They’re giving you false or incorrect information (this should be a huge red flag).

If an applicant has bad credit or no credit, there are a few options that can help them get approved while giving the landlord some peace of mind:

- Applying with a cosigner: Having a trusted family member with stronger credit cosign with the applicant can improve their approval ratings.

- Larger security deposit: Putting down a larger deposit (1.5-2x usual deposit) is a common strategy for applicants with poor credit.

- Prepay rent: Another extra payment option is to prepay the first and last month’s rent in advance.

- Longer initial lease term: Agreeing to a longer lease period provides some extra stability that can offset credit issues.

Assessing rental applications based on the whole story instead of just the credit score isn’t just an act of generosity. In some situations, blanket “no credit, no rent” bans can open you up to Fair Housing Act violations. This is also why it’s important to document alternative arrangements consistently across applicants.

Detect Fake Pay Stubs with Snappt

Roughly 10% of rental applications contain fraudulent documents. This is a growing problem that credit checks alone often can’t catch. That’s why TenantCloud partners with Snappt, the leading AI-powered fraud detection platform for rental applications.

Snappt’s document-based verification analyzes documents such as pay stubs and bank statements, and using advanced AI, can quickly detect alterations and fabricated documents that might pass human review. Our AI-powered analysis verifies pay stubs and bank statements with 99.8% accuracy.

Best of all, Snappt is available as an ad-on to TenantCloud’s Full Check screening package. Get credit reports delivered as a printable PDF within hours, available to both the landlord and applicant for 30 days.

Steps to Take Before Rejecting a Tenant Based on Credit

No landlord enjoys rejecting a rental application, but sometimes it’s necessary to protect your investment. Credit is only one indicator, though, and doesn’t always tell the full story. Here are a few steps you should take before rejecting an application on the basis of credit:

- Ask the applicant directly about any concerning items on their report. Factors outside of their control, like medical debt, job loss, or divorce, often explain bad credit.

- Contact previous landlords to add some context to the applicant’s rental history.

- Consider mitigating factors like stable employment, strong references, and high income.

- If you do decide to deny the application, be sure to send an adverse action notice with the credit bureau’s contact info and dispute rights.

- You might also consider consulting a legal professional to make sure you’re not violating any laws by rejecting the application.

Legal Compliance and Best Practices for Tenant Credit Checks

Now that you know how to run a credit check on a tenant, there are a few regulations surrounding tenant credit checks you need to know. These laws help prevent discrimination and protect renters’ rights. Here are a few best practices to help you ensure legal compliance:

- Per the FCRA, written consent is required before pulling any report.

- Provide adverse action notices if you reject an application based on credit.

- Apply screening criteria consistently across all applicants

- Some jurisdictions, like Oakland and Philadelphia, restrict the use of credit scores for Section 8 or subsidized housing applicants.

- Some areas prohibit automatically rejecting an application based on credit score alone (Kansas City has this rule, for example).

- Keep all credit reports stored securely and confidentially.

- Include the credit bureau’s contact information, and inform applicants of their right to dispute information.

Run Smoother Credit Checks

If you’re curious how to run a credit check on a tenant yourself, try a property management software with built-in screening tools. TenantCloud offers flexible, secure credit and background checks for landlords that can be run right from an application.

Start managing properties with ease. Try TenantCloud free for 14-days.

Frequently Asked Questions About Tenant Credit Checks

How much does it cost to run a credit check on a tenant?

Credit check costs typically range from $25-$45 per applicant. Full screening packages, including criminal background and eviction checks, run $35-$65. This fee may vary based on the screening service used and the depth of the credit inquiry.

Can a landlord run a credit check without my permission?

No, landlords must obtain written permission from the tenant to conduct a credit check. This consent is part of the application process and complies with the Fair Credit Reporting Act (FCRA). When you conduct tenant credit screenings on TenantCloud, our system handles this consent automatically.

What credit score do landlords typically look for?

In 2025, the national average minimum credit score for rentals falls between 620 and 700, but this will depend on your market. For instance, luxury properties in cities like San Francisco typically require 700+, while suburban and rural markets often accept 620-650. For most locations, 650 is the sweet spot that opens doors to most rental properties nationwide.

How is a tenant credit check different from a background check?

A tenant credit check focuses on financial patterns like debt, missed payments, bankruptcies, and credit utilization. A background check, on the other hand, reveals criminal history, convictions/arrests, and legal proceedings like evictions.

Does running a tenant credit check affect their credit score?

Most tenant credit checks appear on your credit history as “soft pulls,” which don’t affect the tenant’s credit score. However, some credit screening services use a “hard pull,” which can temporarily lower your score by a few points.

How long does a tenant credit check take?

How long does a tenant credit check take?