Rental markets are always in motion, but today, the stakes are especially high. The recent market is driven by high interest rates, changing home prices, and affordability concerns. As a result, many tenants are weighing the rent vs. buy debate for longer than they did before. To hold onto great tenants and empower their rental businesses, property managers need to keep this decision-making process in mind.

Understanding what tenants are going through is a strategic advantage. After all, when you send that lease renewal proposal, many tenants are probably wondering if they should continue renting or finally take the leap to buy a home. When you understand how tenants evaluate the situation, you can proactively adjust your prices, amenities, and communication style to retain them.

In this guide, we’ll outline what landlords and property managers need to know about tenants’ mindsets to optimize their rental strategies and maintain high occupancy in 2026. We’ll explain where the rent vs. buy debate stands today and how all-in-one property management software helps you retain your best tenants.

TL;DR

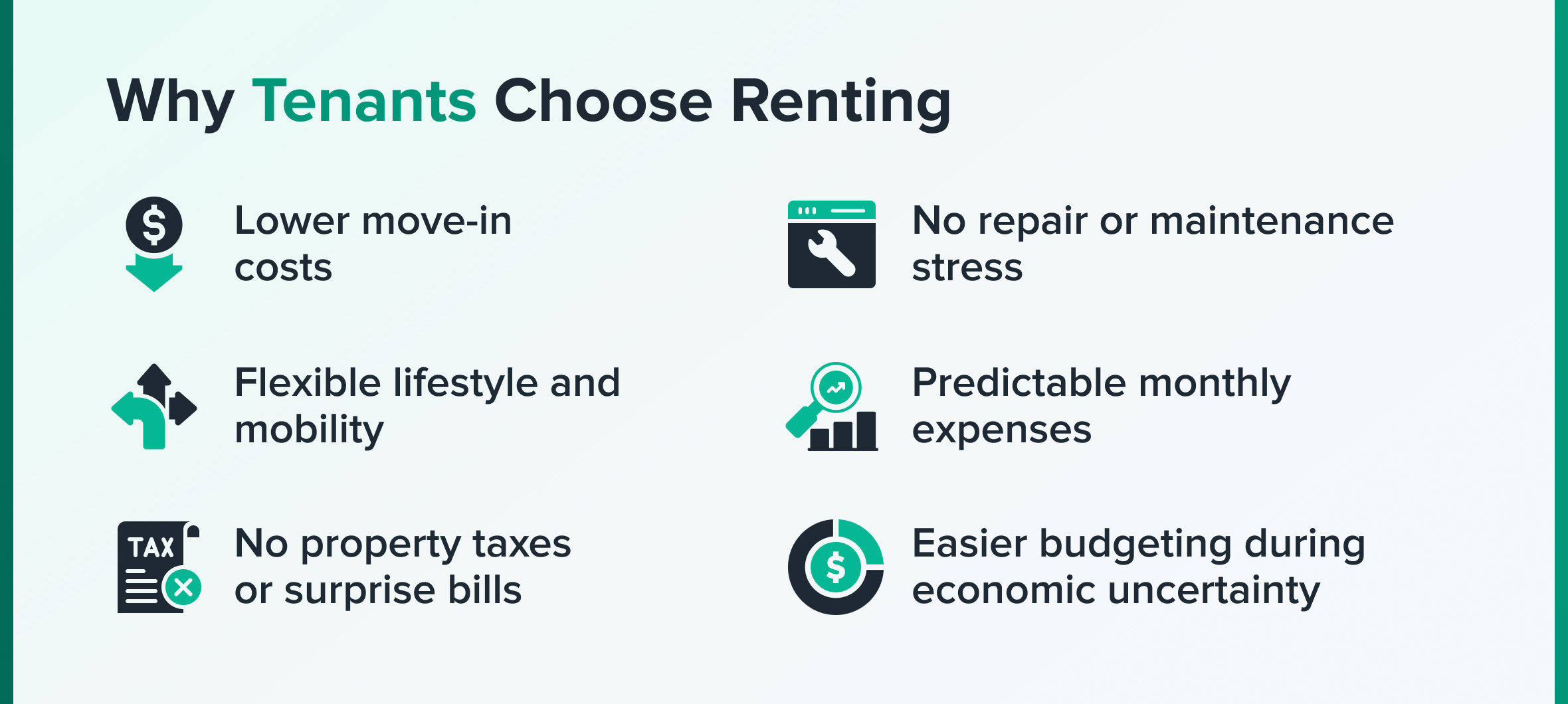

Many tenants considering the rent vs. buy decision are leaning towards renting. Renting means avoiding the high upfront costs, rising property taxes, and continual maintenance that come with homeownership. By renting, they gain more liquidity, freedom, and peace of mind.

As a landlord or property manager, you need to think like a renter to retain your best tenants. Now’s the time to gain a competitive advantage against for-sale homes in your area by pricing strategically. By setting a monthly rent rate that’s better than the costs of owning starter homes in your area, you can retain tenants who are considering a purchase.

When marketing your listings, make sure to highlight the advantages of renting, including maintenance-free living and lower upfront costs. Many landlords also incentivize renewals by offering small savings or bonuses.

However, the real difference lies in creating a seamless rental experience. Property management software removes friction and makes a tenant’s life easier. By streamlining everything from repairs to communication, all-in-one platforms are the best way to keep your tenants happy — and in your unit for years to come.

While tenants are constantly considering their best move, landlords should stay one step ahead by understanding renters’ mindsets. The bottom line? Always consider rent versus buy to improve your operations and ROI, especially in 2026.

The Current Landscape: Rent vs. Buy Market Dynamics

For many renters, rent or buy isn’t a choice with a lot of freedom. In major metros with high prices and low supply, the decision is tilting towards renting. It’s not because tenants don’t want to own a space of their own anymore, but it’s because homeownership is becoming harder to justify, save for, and achieve.

Mortgage interest rates have stabilized compared to recent years and are predicted to drop to 5.75%. However, there are still major affordability challenges that make it harder to reach the goal.

Property taxes are rising, and the cost of ownership is creeping up. Insurance premiums, property maintenance, and repairs are becoming more expensive with inflation. While rental owners can access tax deductions for landlords, homeowners who use the property as their primary residence don’t have the same access to tax savings.

As a result, most renters find leasing to be a safer, more realistic alternative. Renting properties offers more flexibility, less upfront costs, and fewer surprises. They don’t have to make a major long-term commitment or come up with $30,000 for the down payment.

Additionally, renter demographics are rapidly evolving. Gen Z added 6.7 million households to the 2026 rental market; they now account for 23% of renters. Together with Millennials, the younger generations tend to delay homeownership in response to affordability barriers.

All things considered, long-term renting is becoming the norm for many renters across the U.S. While landlords are competing with the idea of homeownership, more and more tenants are choosing the flexibility and affordability of renting.

Inside the Tenant’s Mind: How They Use a Rent vs. Buy Calculator

Because money matters are at the forefront of real estate concerns, many tenants turn to a rent vs. buy calculator to get more insight into the cost comparison. These online tools help prospective buyers gauge the real monthly and long-term costs of owning a home versus renting a unit.

While they help renters find what makes the most sense for them, they also give landlords insight into what tenants are thinking. More importantly, it tells landlords what may encourage tenants to leave their unit and kick off their homebuying journey.

These calculators examine many variables, including:

Opportunity Costs

Buying a home locks funds into a property, meaning buyers can’t access their money easily or invest it elsewhere, like the stock market. If a tenant took their down payment and invested it in another asset rather than putting it in home equity, how much would it earn?

Depending on the market and circumstances, many renters would rather wait to buy a home if it means higher returns from other avenues.

Down Payments

When buying a home with a mortgage, buyers have to put a lump sum down upfront, which typically ranges between 3% and 20% of the property’s price. The more you put down, the lower your mortgage balance is. However, coming up with thousands of dollars causes delays for many buyers looking to enter the market.

Closing Costs

Buying a home involves unrecoverable costs and surprise fees. To finalize the purchase, tenants must pay a fee of 2% to 5% of the purchase price. Based on the average home sale price in the U.S. of $405,300, as of Q4 2025, closing costs could range from around $8,106 to $20,265.

When you add this to the down payment and monthly mortgage cost, many renters view leasing as an affordable alternative without the upfront expenses.

2026 Mortgage Rates

As of April 30, 2026, the 30-year fixed-rate mortgage averaged 6.30%, while the 15-year fixed-rate averaged 5.64%. Even though interest is lower than before, it still adds a significant amount to the monthly bill. Depending on the market and the tenant’s financial circumstances, tenants may be able to rent a comparable home for less than their monthly mortgage bill.

Property Taxes and Insurance

Both tax rates and insurance prices are on the rise, especially in major metros. Tenants may not be ready to take on these additional costs that come with homeownership.

Maintenance and Repairs

Renters don’t have to worry about the annual costs of property maintenance, but as owners, they’d probably pay between 1% and 2% of the home value every year. Many tenants prefer the easy, hands-free maintenance experience that comes with having a landlord.

All in all, rent vs. buy calculators shine a light on the total costs of homebuying. They help tenants plan their next move and make an informed decision about what they can actually afford.

As a property owner, you can run a rent vs. buy calculation yourself to determine the best price for your listing — keeping your unit competitive against local starter homes. If you’re able to offer a better price than for-sale properties in your area, you’re more likely to retain tenants who may be thinking about buying their first home.

Marketing the ‘Rent’ Advantage to Prospective Tenants

When you’re marketing your available units, don’t think that other rentals are your only competition. Create a strong case against properties up for sale by highlighting the hidden, unrecoverable costs of homeownership.

Remember, today’s tenants are running the numbers and constantly weighing the rent vs. buy decision. Most of the time, buyers underestimate how much they’ll actually end up paying to make the purchase.

We recommend making the costs clear and straightforward in your positioning by adding this type of language to your marketing materials:

“Don’t spend $10K+ in closing costs, unpredictable repair bills, and other homebuying fees. Instead, move in with one simple deposit. No surprises. Less stress. More money in your pocket.”

Another key point to highlight is maintenance-free living. Tenants don’t have to deal with the back-and-forth coordination that comes with scheduling a repair. After all, what tenant wants to deal with a sudden bill of $9,000 when an HVAC needs replacing? And who wants to worry about what landlord insurance covers and its cost? In 2026, this is a major selling point to win over renters due to skyrocketing contractor and repair costs.

Overall, we recommend promoting the best parts of the rental lifestyle: flexibility, liquidity, and mobility. These benefits appeal to younger renters who prioritize freedom, adaptability, and financial agility.

Tenants are always asking themselves, “Does renting make sense right now?” Be there to answer them. Show them that a rental property is more than just a place to call home. It’s a smart financial decision that reduces stress, simplifies their life, and saves them money.

Retaining High-Quality Tenants in a Competitive Market

If you have responsible, rent-paying tenants who take great care of their property, you don’t want to lose them if they make the jump to homeownership. Here are a few strategies and incentives the pros use to get them to stick around:

1. Reward tenants for renewing the lease with a small rent credit or even a $50 Amazon gift card.

2. Invest in property upgrades and premium amenities to enhance their experience without added overhead.

3. Maintain excellent landlord-tenant communication to provide five-star service.

4. Leverage modern smart home technology that rivals the appeal of starter homes.

Streamline Your Portfolio with the Right Tools

Beyond marketing best practices and renewal incentives, your day-to-day workflow can also work in your favor. By managing your units efficiently, you can keep costs down while improving your tenant satisfaction. Offering a smooth, low-friction experience becomes a part of your overall value proposition. That’s where property management software comes in.

All-in-one software offers a centralized platform for rent collection, maintenance requests, and tenant screening. By keeping everything organized and in one place, you avoid delays, human errors, and other headaches.

While you enjoy less manual work, you offer tenants convenience. Property management software creates a smooth, easy, and modern renting process that tenants appreciate. Landlords who use it appear more professional and reliable, giving them a competitive advantage over other similar listings.

Tenants feel the difference when you respond to maintenance requests faster, practice transparent communication, and make it easy for them to pay rent online. A seamless rental experience encourages tenants to continue renting and stay in your unit for the long run.

Conclusion

In today’s market, rent vs. buy isn’t just something for tenants to worry about. It should be top of mind for landlords and property managers, too. Understanding renters’ considerations, motivations, and financial positioning helps you speak to tenants who are on the fence about what to do.

When you think like a tenant, you're more likely to address their actual concerns. As a result, you can practice smarter marketing and offer incentives that improve your retention.

Overall, buying a home or continuing to rent is a deeply personal decision. Both factors have upsides and downsides. More tenants are choosing to delay homebuying due to affordability and convenience, especially in major metros.

If you want to retain tenants who aren’t sure about whether to rent or buy, efficient management is one of the most effective strategies you can practice. To optimize your rental business and keep tenants happy for longer, start using a leading property management software. In 2026, all-in-one software creates a modern, easy, mobile-friendly tenant experience that stands out from the crowd.

Ready to offer more value than rentals and for-sale properties in your market? Sign up for TenantCloud today to streamline operations so tenants will want to renew, year after year.

Rent vs. Buy FAQs

Is it financially better to buy or rent?

The decision to rent vs. buy depends on the tenant’s specific situation. If tenants have the available cash to use as a down payment and are looking for a long-term wealth-building strategy, buying a home can be a solid choice. However, it depends on the local market conditions and the ability to afford the unexpected costs of ownership, such as repairs and taxes.

On the other hand, renting offers a more affordable and flexible alternative. Renters avoid the upfront costs of buying a home as well as the ongoing maintenance expenses and surprise bills. In big metros and high-interest-rate markets, renting is often the better financial choice for tenants in 2026.

What is the 5-rule rent vs. buy?

The 5% rule helps renters decide whether it’s smarter to rent or buy. It considers the unexpected and unrecoverable costs that come with purchasing a home. Beyond the monthly mortgage bill and the initial down payment, buyers are also responsible for paying interest, taxes, and maintenance costs.

The 5% rule states that if the unit’s monthly rent is less than 5% of the home price divided by 12, renting is smarter. If the rent amount is more than 5% of the home’s price divided by 12, buying may be a better financial move.

For example, let’s say a buyer is considering a $600,000 home. 5% of $600,000 is $30,000. Divided by 12, that’s $2,500 per month. If they’re able to rent a comparable property for less than $2,500, renting is their best bet.

As a landlord, consider the 5% rule when setting your rent price to attract renters who are running the same rent or buy calculation.

What is the 2% rule in rental property?

The 2% rule helps landlords and property managers set a profitable rate for their rental properties. The rule states that the monthly rent should be at least 2% of the property’s total purchase price.

What salary to afford a $400,000 house?

As a rule of thumb, the total housing costs should be within 30% of the buyer’s monthly income. But in 2026, the salary threshold also depends on the down payment amount, current interest rates, and the amount of debt the buyer has.

For example, if buyers put down a 25% down payment on a $400,000 house, they’d require a lower salary than if they only put 5% down. Similarly, if they have large debts that cut into their income, they’d need a higher salary than someone without that extra financial burden.